J&K Bank 09 months profit grows 43% to 250Cr, 103Cr in Q3

Bank’s total business as on the close of December 2018 stood at 1, 57, 279Cr

Srinagar: JK Bank, the state-owned premier financial institution announced its results for the quarter and nine months ending December 31, 2018, after the reviewed results of the Bank were adopted by the Board of Directors.

The Bank reported a 43% increase in its net profit to Rs 250.09 Cr for the three quarters ending December 31, 2018, as compared to Rs 174 Cr reported for the same period in previous fiscal.

For the third quarter, the bank posted a profit of Rs 103.75 Cr as compared to 72.47 Cr for the same quarter last year.

The growth in J&K Credit has been reported at 22% over the last year and net interest income the difference between interest earned on loans and that paid on deposits grew to Rs 2452 Cr as compared to Rs 2215 Cr in the nine months period for last financial year.

Expressing satisfaction on the results Parvez Ahmed Chairman and CEO JK Bank said in the official communiqué, “The Bank has been able to maintain consistency in its growth rate and earnings. Our focus on the expansion of credit in Jammu and Kashmir has strengthened our core income with a credit growth rate of 22 % which is spread across all the regions of the state with traction in all the sectors especially retail and SME.”

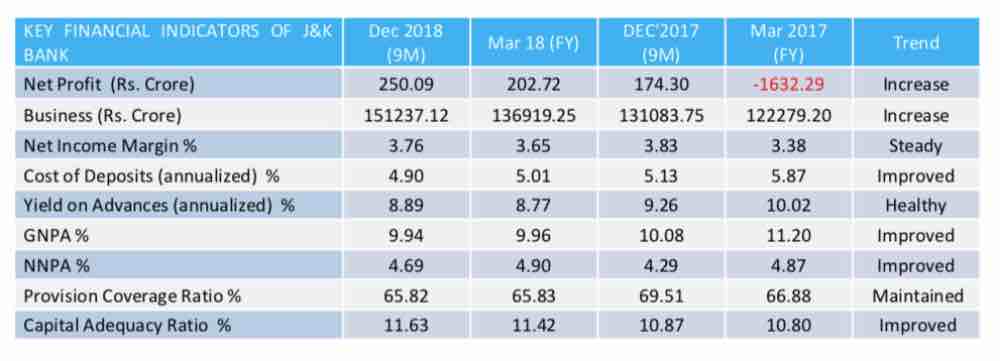

JK Bank, Key Financial Indicators.

He added, “We met our third-quarter profit estimates despite downgrading the much publicized IL&FS exposure and making adequate provisions, though a number of the banks are still maintaining the account as standard. With this our clean up is almost complete and recognition cycle is drawing to an end though credit costs will take some more quarters to align to the long term averages due to provisioning pressure on account of IL&FS and ageing of NPAs. Going forward we are going to consolidate further and for now we will maintain our strategy of J&K state focused growth which offers a reasonably high absorption capacity with pull across sectors in alignment with the development oriented budget and recently announced an industrial policy of the state.”

“I believe this is our resilience getting visible with unflinching support from our promoters the state government, guidance from the Board, loyalty of our customers, emotional equity of our people and consistent efforts from the dedicated human capital of the bank who have done a commendable job during the turbulent times over the last two years. From now onwards, the bank will focus on the transformation exercise by aggressively implementing the Business Plan 2022 prepared in consultation with management consultants and we expect the implementation to be complete by the end of FY 20,” she said.

“Some of the initiatives have already been either rolled out or piloted and have shown very encouraging results. Especially in the digital space, our share of digital transactions has increased to 60% besides the digital acquisition of personal loans through our Phone Pe Loan channel has grown exponentially. Post-transformation we are envisaging a total business of 2.45 Lac Cr with a targeted profit of Rs 2000 Cr, NIIM ranging between 3.5-4%, ROA of 1.3%, ROE of 16% and credit cost below 1% at the end of FY 2022. So in terms of numbers, our best is yet to come” added Parvez Ahmed.

“We will also focus on expansion of our franchise with a mix of full-fledged Business Units and the innovative micro version Easy Banking Units to map the whole geography in J&K state especially in the hitherto underbanked rural pockets of the state on the lines of our initiative in Ladakh where we opened 35 Easy Banking units to link all the 111 villages of the Leh district. This is going to strengthen our already strong CASA of 49% and democratization of credit availability in the rural areas from the now urban-centric credit concentration of Jammu & Srinagar cities. Simultaneously as I said earlier too, we are optimizing our presence in the rest of India by expanding our retail & niche business in territories where we have a strong franchise,”added the Chairman.

“We see a lot of potential for increased lending in sectors of SME, Tourism Infrastructure, Agriculture & Allied, Infrastructure(Government Spending), Home Loan, Personal Finance to government employees, Horticulture, Gold Loans etc. within the state having a prospect of adding Rs 11000 Cr in the near term. Promoting the startups and new entrepreneurs remains our priority area as we go deeper in the geographies in congruence with the policy support for startups at the state and central government level and we will act as an enabler for the bright youths of our state” asserted Parvez Ahmed.

The bank’s total business as on the close of December 2018 stood at 1, 57, 279 Cr comprising of deposits of Rs 86,210 Cr and gross advances of Rs 71,069 Cr as compared to 1,36,936 Cr a year ago registering an increase of around 15%. The Bank reported a stable Net Interest Margin (NIM) of 3.76% largely driven by the bank’s low cost of funds at 4.90% with a CASA contribution of 49%. The NPA coverage ratio though static on a YOY basis and still comparable with the best in the industry, has seen a dip on sequential basis to 65.82 % mainly on account of downgrade of the IL&FS which reflects that the bank has been able to tide over the IL&FS shock without any major deterioration in the balance sheet parameters. The Gross and Net NPA ratios of the bank by and large remained unchanged at 9.94% and 4.69%.

Discussing about the problem of NPAs Chairman JK Bank said,”Right from the word go I have tried to instill transparency by recognizing the stressed accounts in the balance sheet which were at that time professed at a very high level of 20% and the slippages of 13,000 Cr including that of IL&FS are from the inherited portfolio. Having done that we took initiatives for cleansing & consolidation of Balance Sheet, Recovery and Resolution of Bad Debts by making adequate provisions, Creation of a dedicated Impaired Assets Portfolio Management (IAPM) vertical to focus on recovery, settlement and resolution of NPAs which resulted in Recovery/Resolution of about Rs. 5000 crore bad debts with improved Provision Coverage and net NPA ratios. Simultaneously we de-prioritized corporate especially low-rated and Consortium lending and enhanced our focus on Retail and MSME particularly in productive sectors of J&K state.”

He added, “so we have been able to recognize and manage our NPAs fairly well and the latest surprise NBFC fiasco of IL&FS leading to a major downgrade in the current quarter is also now behind us. With this we have completed the transparent asset recognition cycle which had culminated in a loss of Rs 1632 Cr for the FY 16-17 with a sharp dip in our Provision Coverage Ratio. The Bank has shown a strong resilience with a focused approach in NPA management and earnings growth by expansion of credit in J&K state. The good news all along has been that our J&K state rehabilitated portfolio has behaved very well with just 1% slippages over the last one year.”